Corrs venture capital and tech M&A update - June 2026

Welcome to the June 2026 edition of the Corrs venture capital and tech M&A update, a quarterly publication which highlights recent key developments in the Australian venture capital and tech M&A market and upcoming changes to watch out for.

Kind regards

Corrs Corporate/M&A Team

Cut Through Venture (CTV), in partnership with Corrs, recently released its Australian Venture Capital Funding Report for Q1 2026. The report highlighted that many of the biggest investment rounds are going to startups focused on space, defence, robotics, AI infrastructure, cybersecurity, biotech and climate.

Key capital raising statistics

The Australian startup capital raising statistics in CTV's report show:

Sector perspectives

In terms of sector-specific data, the CTV report shows that, for Q1 2026:

Investor sentiment and outlook

CTV's investor sentiment survey indicates that investors are being more selective about the startups and market segments where they believe defensibility exists, but the overall sentiment continues to be largely positive:

While patents can be an important form of IP protection for many tech startups, there has been a long-running dispute about whether software inventions can be patented in Australia. The High Court has now settled the debate, opening the door for software-based innovations to be patented.

Earlier this year, the High Court refused to hear an appeal in a landmark case between Aristocrat Technologies and the Commissioner of Patents (Commissioner). The High Court took the view that the Full Federal Court's earlier decision in favour of patentability was clear and did not merit reconsideration. For technology companies and their investors, the outcome is a significant positive signal: it is now clearly established law that computer-implemented inventions can qualify for patent protection, even if they use conventional, off-the-shelf computer hardware, provided they do more than implement an abstract method or scheme.

The dispute had a long and unusual history. In 2021, the Full Federal Court applied a two-step test requiring computer-implemented inventions to demonstrate an "advance in computer technology" to be patentable – a high bar that effectively excluded many software-based innovations. An initial appeal to the High Court in 2022 resulted in a rare even split among six judges, leaving the matter unresolved. When the case returned to the Full Federal Court in 2025, the court rejected the "advance in computer technology" requirement and replaced it with a more flexible test: whether the invention produces an "artificial state of affairs and a useful result." In February 2026, the High Court refused to hear the Commissioner's further appeal, describing the Full Court's conclusion as an application of "established principles" that was "unanimous and clear."

The position is now settled: the test, under Australian patent law, is whether the invention, as implemented, produces an artificial state of affairs and a useful result. This means that a novel idea implemented on a computer to achieve something useful can be patentable, even where the underlying hardware is standard, provided it involves more than mere manipulation of an abstract idea. IP Australia has since updated its Patent Manual to align with the decision.

This broader and more certain scope for software patents means founders building software-driven products can more confidently pursue IP protection for their innovations, strengthening their competitive position and making their businesses more attractive to investors. Equally, they will need to be mindful of the potential infringement of third-party patent rights and should undertake clearance searches to ensure freedom to operate. For venture capital investors conducting due diligence, the decision clarifies the legal landscape and reduces uncertainty around the enforceability of software patent portfolios in Australia.

Shareholders' agreements governing VC-backed companies frequently contain confidentiality restrictions, pre-emptive rights on share transfers, affiliate or permitted transferee regimes, and compulsory transfer provisions triggered by default. These provisions were central to a recent dispute heard in the Supreme Court of NSW. For startups, this case underscores the importance of having well drafted documents and a thorough understanding of the obligations within them.

Background

On 29 May 2026, Justice Hammerschlag delivered judgment in Dexus Capital Investment Services Pty Ltd v Australia Pacific Airports Corporation Limited [2026] NSWSC 600, a complex shareholder dispute concerning Australia Pacific Airports Corporation Limited (APAC), the owner of Melbourne Airport and Launceston Airport. APAC is privately held by five institutional investors and investment managers, with Dexus managing interests totalling a 27.32% stake (collectively, the Dexus Bloc), alongside IFM Investors (25.17%), Future Fund (20.34%), SAS Trustee Corporation (managed by TCorp) (18.47%) and Utilities Trust of Australia (managed by HRL Morrison & Co) (8.70%).

The relationship between the APAC shareholders is governed by a shareholders' deed (the Shareholders' Deed). The members of the Dexus Bloc had agreed that their rights, powers or discretions may only be exercised by Dexus for and on their behalf.

In late 2023, Dexus commenced 'Project Mercury' to sell a 9.7% interest in APAC. During the sale process, Dexus gave around 130 people, including prospective bidders and their advisers, access to a virtual data room containing APAC's business and financial information, including the highly sensitive APAC 20-year financial forecast model, without APAC's knowledge or consent. The Shareholders' Deed required that confidential information only be disclosed to a prospective purchaser that had entered into a confidentiality deed with the other shareholders in a form reasonably satisfactory to them and enforceable by any of them. Dexus instead used a template confidentiality deed that it believed had been previously agreed with APAC, and entered into side letters amending some of those deeds. In May 2025, the APAC Board issued a default notice to Dexus asserting a material irremediable breach of the Shareholders' Deed, triggering the compulsory divestment process for the entire Dexus Bloc's 27.32% holding.

Outcome

The NSW Supreme Court held that:

Justice Hammerschlag ordered that all claims by Dexus are dismissed. The significant practical impact is that, subject to any appeal, Dexus will be forced to sell its A$4.5 billion stake in APAC to the other shareholders.

Takeaways

The judgment provides several important observations:

Australia's technology, media and telecommunications sector faces significant regulatory reform in 2026, with major implications for technology companies, startups and their investors.

Online safety obligations

In December 2025, the Online Safety Amendment (Social Media Minimum Age) Act 2024 (Cth) took effect, requiring services that enable online social interaction to take reasonable steps to prevent users under the age of 16 from holding accounts, including through age-assurance technologies. Separately, online safety codes and standards now apply to a broad range of online services on a risk-tier basis, targeting both unlawful content (Phase 1) and age-restricted material (Phase 2). The Phase 2 'Age-Restricted Material Codes' aim to protect Australian children under the age of 18 from seeing material that is 'lawful but awful', including pornography and self-harm material. Full Phase 2 compliance was generally expected by March 2026.

Privacy and Data Protection

The Office of the Australian Information Commissioner (OAIC) is conducting a sector-specific sweep of privacy policies across approximately 60 businesses in high-risk, face-to-face data collection environments (e.g. pharmacists and car dealerships) in response to overcollection risks. The focus of the sweep aligns with the OAIC's broader enforcement priorities for 2025-26, including correcting power and information asymmetries and scrutinising technologies such as biometrics, facial recognition and pixel tracking.

Additionally, from 10 December 2026, businesses using personal information in automated decision-making (ADM) that could reasonably affect individuals' rights or interests must, in accordance with newly introduced Australian Privacy Principles, disclose in their privacy policies the personal information used in the ADM and the decisions made by the ADM. Regulators are likely to require more detailed evidence regarding the operation of ADMs, and organisations should therefore be able to map automated processes, document data inputs and decision logic and provide precise disclosures consistent with the statutory requirements.

Surveillance

Australia's surveillance regime is a complex patchwork of Commonwealth and state laws, with active reform progressing at both federal and state level. Facial recognition technology remains a particular regulatory focus, given that it involves the collection of biometric data, which is classified as sensitive information under the Privacy Act, and therefore attracts a heightened risk profile due to the significant potential consequences for individuals if mishandled.

Spam Compliance

Australia's Spam Act 2003 (Cth) (Spam Act) prohibits the sending of commercial electronic messages without the recipient's consent, without identifying the organisation and without an opt-out option. The Australian Communications and Media Authority (ACMA) is actively enforcing this and imposing substantial penalties.

ACMA's 2025-26 enforcement priorities include disrupting mobile number fraud and combatting spam and telecommunications scams. In 2026, ACMA has already issued a A$376,200 penalty and accepted an 18-month enforceable undertaking against a telecommunications company for failing to carry out anti-scam identity checks which resulted in consumer losses of at least A$175,000. Additionally, from 1 July 2026, branded text messages displaying an organisation's name at the top of such messages will need to have the sender ID registered on the SMS Sender ID Register as part of the Australian government's 'Fighting Scams' initiative.

Businesses should re-evaluate commercial electronic messages and review the validity of their customers' marketing consents on an ongoing basis to avoid the risk of increased Spam Act enforcement.

Read the full Corrs Article on TMT trends 2026: cyber security and online safety.

Read the full Corrs Article on TMT trends 2026: privacy, surveillance and spam.

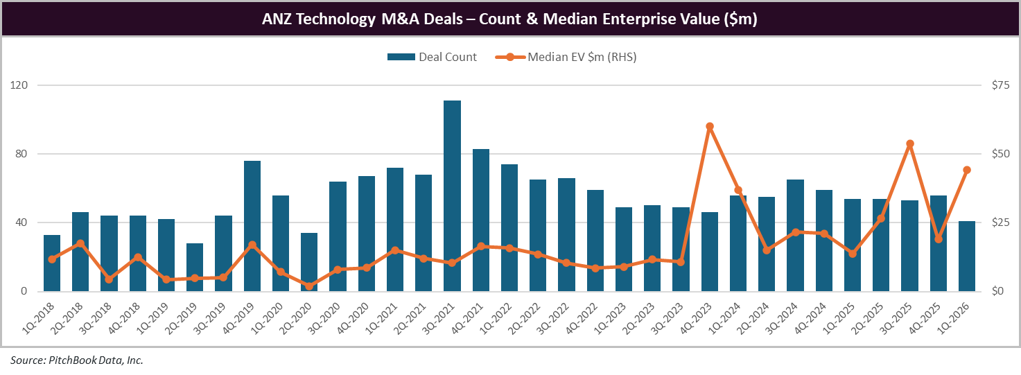

Platform Advisory Partners' analysis of Australia and New Zealand (ANZ) technology M&A deals from Q1 2026 highlights the following.

Despite a slight downturn in deal volumes, continued overseas interest in Australian technology businesses has seen local median transaction sizes tick upwards, with the majority of targets in Q1 2026 A$100 million+ deals (listed below) finding new overseas homes:

A range of external factors affected SaaS valuations in the first quarter of 2026, including the 'SaaSpocalypse' resulting from AI advances, ongoing impacts from tariffs and the uncertainty resulting from conflicts in the Middle East. This has ultimately seen SaaS revenue multiples decrease from a median over 5.0x to 3.4x in only a few months.

These global trends have filtered down through the ASX boards as well, with local technology leaders in Xero, WiseTech and Pro Medicus collectively seeing A$50 billion in market cap wiped over the past six months. Continued multiple compression on SaaS large-caps will likely see sustained pressure on technology deal counts across ANZ, as bid-ask spreads widen until targets learn to accept 'new normal' valuation multiples, or until macro factors improve and multiples expand once again.

Platform Advisory Partners is a Melbourne based advisory firm specialising in providing M&A and capital raising advisory services to high-growth and technology companies.

Corrs is a leading Australian independent law firm, with a cross-disciplinary team which has a deep understanding of the needs of startups and high growth companies. We act for both startups and a range of investors, including local and international venture capital funds, strategic investors and universities.

Corrs has also developed CorrsEdge, a cutting-edge online platform which gives startups the legal support they need at the early stage of their growth cycle. The platform offers access to over 30 intelligent legal documents with dynamic automation capabilities which enables users to generate bespoke documents and tailor them for their business. The Corrs Edge platform saves time and money, allowing startups to ensure that they have high quality legal documents without the typical costs of using a top tier law firm.

This publication does not constitute legal advice and should not be relied on as such. You should seek individualised advice about your specific circumstances.